In the world of luxury timepieces, few names command as much respect as The Swatch Group AG. Yet, beneath the elegant façade of Swiss craftsmanship lies a ticking economic challenge, Donald Trump’s newly announced 39% tariffs on Swiss exports. Dubbed a financial tsunami for the watch industry, these tariffs are more than just a blip on the economic radar; they represent a potential seismic shift for Swatch, one of the leading players in the global market. By dissecting the implications of these tariffs, we can uncover what this means for Swatch stock, its investors, and the broader luxury goods landscape.

Consider this: As Swatch’s stock currently trades at 144.9 CHF, it has already seen a worrying year-to-date decline of 9.41%. When juxtaposed against a fair value estimate of just 95.2 CHF, there’s a glaring overvaluation that savvy investors cannot ignore. With an EPS of 1.19 CHF, a book value per share of 233.97 CHF, and a company size of 6.83 billion CHF, Swatch seems robust on the surface. However, a deeper dive reveals a more complex image, one where Trump tariffs could substantially alter demand patterns, steering consumers towards more affordable alternatives or the burgeoning secondhand market. As we navigate this unfolding scenario, join us in exploring detailed insights into Swatch stock—a pivotal analysis steeped in both opportunity and risk.

Impact of Trump’s % Tariffs on Swiss Exports

Donald Trump’s sudden imposition of a 39% tariff on Swiss exports sent shockwaves through the global luxury goods sector. From a policy standpoint, these duties effectively serve as a punitive surcharge aimed at discouraging U.S. consumers from purchasing high-end Swiss products, a sector dominated by precision-driven manufacturers like The Swatch Group AG. The direct result is a material cost increase on every timepiece imported into the U.S., transforming price-sensitive purchases into economic gambles for American buyers. This “Trump Tariffs Swatch stock” scenario raises immediate concerns about how these added costs will be absorbed, by end consumers, retailers, or directly by the company itself.

America constitutes one of Swatch’s largest export markets, accounting for roughly 20% of global sales. Prior to the tariffs, the U.S. appetite for mid-range Swiss watches had been growing steadily at an annual rate of approximately 5–6%. Now, with an elevated price floor, many aficionados may pause or defer purchases, disrupting a reliable revenue stream. Meanwhile, competitors from countries not subject to tariffs, such as Japan or Germany, may exploit this window to undercut Swiss makers on price. In essence, what began as a geopolitical maneuver could quickly morph into a market share battle, challenging Swatch’s dominance and prompting investors to reconsider the near-term outlook of “Swatch stock analysis 2025.”

Implications for Swatch’s Market Position

The new 39% levy threatens to undermine Swatch’s carefully constructed brand hierarchy. From entry-level Swatch models to the high-end Breguet and Blancpain collections, all segments will face an abrupt cost escalation in the U.S. market. While luxury consumers may exhibit loyalty, mid-tier aficionados, who drive much of Swatch’s volume—are particularly sensitive to price hikes. With Trump Tariffs Swatch stock sentiment cooling, niche competitors and smartwatches are positioned to nibble away at Swatch’s mid-range foothold.

On a strategic level, Swatch’s response will be pivotal. Will management absorb part of the tariff to maintain price stability? Or will they pass the full burden onto dealerships and end consumers, risking volume contraction? An alternative route could be to double down on digital channels and direct-to-consumer sales abroad, offsetting U.S. losses. Yet, any pivot demands capital investment and time—luxuries that investors monitoring Swatch stock analysis 2025 may not readily afford. Overall, these tariffs recalibrate the competitive playing field, forcing Swatch to adapt swiftly or cede ground to more agile rivals.

Evaluating Swatch Stock Performance

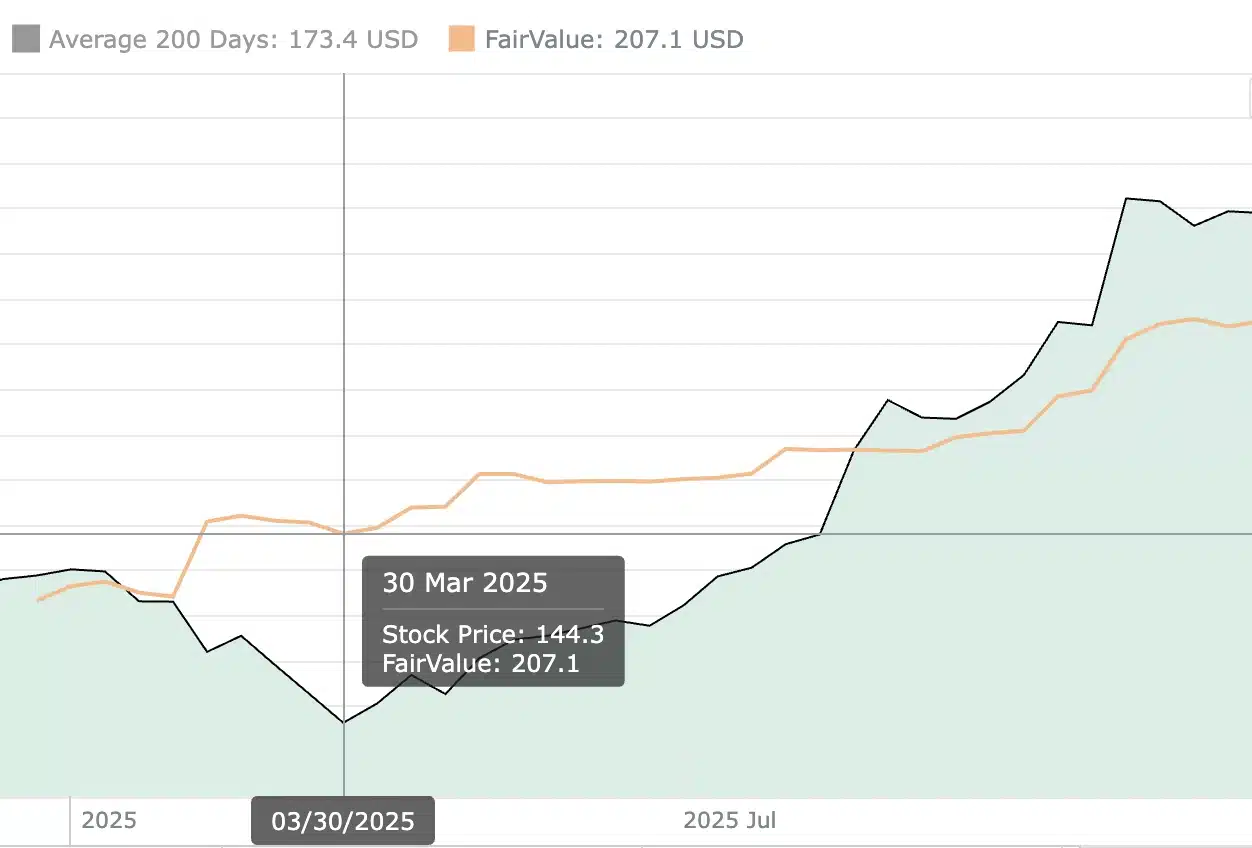

Swatch stock currently trades at 144.9 CHF, marking a year-to-date decline of, 9.41%. Technical and fundamental scores are both weak, each rated 1 out of 5, reflecting diminishing momentum and stretched valuation metrics. However, the company still posts an AI-driven optimism rating of 7 out of 10, hinting at potential macro-economic tailwinds if interest rates ease or consumer confidence rebounds. Investors should note that these mixed signals necessitate a granular Swatch stock analysis 2025 to balance hope against hard data.

From a chart perspective, the break below key support levels around 150 CHF has triggered short-term bearish momentum. Volume spikes on down days suggest heavier selling pressure, likely driven by institutional repositioning ahead of tariff implementation. Yet, rallies above 155 CHF encountered stiff resistance, indicating reluctance among buyers to re-enter without clearer sightlines on policy impacts. Technically, a sustained move back above 150 CHF would be needed to stabilize price action, but until then, Swatch shares remain vulnerable to headline risk and further sell-offs.

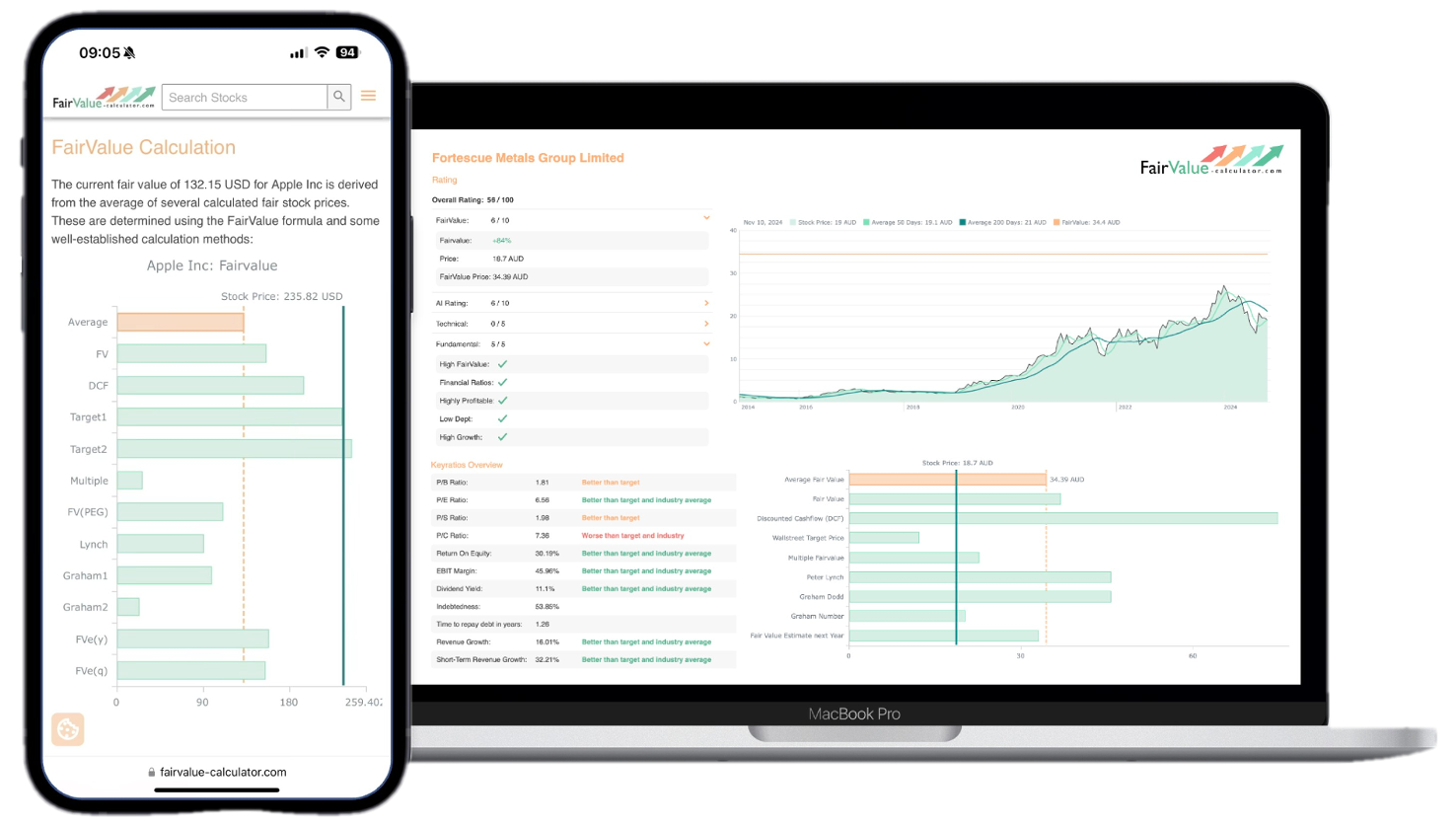

Explore our most popular stock fair value calculators to find opportunities where the market price is lower than the true value.

- Peter Lynch Fair Value – Combines growth with valuation using the PEG ratio. A favorite among growth investors.

- Buffett Intrinsic Value Calculator – Based on Warren Buffett’s long-term DCF approach to determine business value.

- Buffett Fair Value Model – Simplified version of his logic with margin of safety baked in.

- Graham & Dodd Fair Value – Uses conservative earnings-based valuation from classic value investing theory.

- Intrinsic vs. Extrinsic Value – Learn the core difference between what a company’s really worth and what others pay.

- Intrinsic Value Calculator – A general tool to estimate the true value of a stock, based on earnings potential.

- Fama-French Model – For advanced users: Quantifies expected return using size, value and market risk.

- Discount Rate Calculator – Helps estimate the proper rate to use in any DCF-based valuation model.

Factors Contributing to Swatch’s Year-to-Date Decline

Several headwinds predate Trump’s tariff announcement, but they compound its effects. First, Swatch’s revenue growth of 4.1% year-over-year trails the industry benchmark of 8.29%. This slower momentum reflects increased competition from rising smartwatch adoption and a saturated mid-range luxury market. Secondly, the company reported a short-term revenue contraction of –4.86% for the last quarter, whereas peers averaged a 3.55% gain. These dynamics highlight structural challenges even before external shocks.

Further exacerbating the decline is market sentiment around overvaluation. At 144.9 CHF per share, Swatch trades at 12.2x forward EPS, a premium relative to sector peers averaging 10.5x. When you factor in the looming tariffs, analysts argue that any upside is limited under current multiples. In this light, the year-to-date slide is as much a correction of stretched expectations as it is a response to fresh geopolitical risks. Investors conducting a thorough Swatch stock analysis 2025 will weigh these factors to determine if the pullback represents an opportunity or a trapdoor.

Fair Value Estimate vs. Current Stock Price

According to fairvalue-calculator.com, Swatch’s fair value estimate stands at 95.2 CHF—some 34% below its current trading price of 144.9 CHF. This discrepancy underscores significant overvaluation concerns. In a world without tariffs, one might argue for a multiple expansion to close the gap. Yet with a 39% cost surcharge looming, reaching the present valuation becomes even more implausible.

Investors should utilize the Fair Value Calculator tool to stress-test scenarios. For instance, modeling revenue declines of 5–10% in the U.S. owing to price sensitivity can push fair value nearer to 85 CHF or lower. Conversely, if Swatch successfully shifts more sales to markets like China or the Middle East—where tariffs may not apply, the downside may be mitigated. This dynamic variability reinforces why ongoing Swatch stock analysis 2025 is critical: assumptions must be revisited as data on post-tariff demand crystallizes.

💡 Discover Powerful Investing Tools

Stop guessing – start investing with confidence. Our Fair Value Stock Calculators help you uncover hidden value in stocks using time-tested methods like Discounted Cash Flow (DCF), Benjamin Graham’s valuation principles, Peter Lynch’s PEG ratio, and our own AI-powered Super Fair Value formula. Designed for clarity, speed, and precision, these tools turn complex valuation models into simple, actionable insights – even for beginners.

Learn More About the Tools →Financial Metrics: EPS, Book Value, Company Size

Swatch Group’s trailing EPS of 1.19 CHF implies a forward P/E ratio north of 12 when compared to its 144.9 CHF market price. While not exorbitant for a household name, this multiple becomes stretched under earnings pressure. The book value per share sits at 233.97 CHF, yielding a price-to-book ratio of approximately 0.62. Such a discount to book value is unusual for a blue-chip and suggests the market is already pricing in considerable near-term headwinds.

At a group size of 6.83 billion CHF in market capitalization, Swatch is neither a giant like LVMH nor a nimble boutique upstart. It occupies a middle ground that can be both strength and weakness. On one hand, Swatch can leverage scale to negotiate supply costs and invest in innovation. On the other, it lacks the deep pockets of conglomerates to absorb severe demand shocks. These financial metrics frame the debate for “Trump Tariffs Swatch stock” risk versus the pragmatic upside potential should the company navigate this storm successfully.

Shifting Consumer Demand Patterns

Tariffs effectively raise sticker prices for Swiss watches in the U.S., forcing consumers to reassess their purchase decisions. Price-sensitive buyers may pivot to lower-tier models within the Swatch portfolio or seek alternatives from tariff-exempt brands. Others will head to the secondhand market, where gently used timepieces can be had at substantially lower real-world prices. The evolving “Swatch stock analysis 2025” narrative must account for this redistribution of demand across new, used, and non-Swiss segments.

Moreover, demographic shifts accentuate these trends. Younger consumers, who prioritize tech integration and digital connectivity, are already flocking to smartwatches. With tariff-driven price hikes, the appeal of a mechanical Swatch in the $500–$1,000 range diminishes further. Meanwhile, affluent collectors are less price-sensitive but represent a smaller volume. All told, Swatch’s traditional customer base is fragmenting, raising long-term questions about sustainable revenue growth.

Alternative Market Considerations

As U.S. demand decelerates, Swatch must explore alternative markets to offset revenue shortfalls. China, despite trade tensions of its own, remains one of the largest importers of Swiss watches. Strategic partnerships with local distributors or e-commerce platforms could help maintain healthy growth rates above the 8% industry average. Middle Eastern markets, where tariffs may not apply, represent another bright spot, especially for high-end Breguet and Omega lines.

Domestically, the burgeoning pre-owned and certified vintage market offers a backdoor opportunity. Swatch has already shown willingness to enter this segment via authorized resale programs. Expanding these initiatives could capture price-conscious consumers migrating away from full-price new purchases. Supplementing this effort with digital marketing and virtual try-on technology can help Swatch reclaim market share and stabilize its top line during tariff-induced volatility.

Navigating Risks and Opportunities for Swatch Stock

For investors, the interplay between risk and reward in Swatch stock is especially pronounced at the current juncture. On the risk side, tariffs threaten to curtail U.S. revenues by up to 15–20% if consumers balk at higher prices. An overvalued multiple relative to peers amplifies downside potential, especially as technical indicators flash red. Fundamental and technical scores of 1 out of 5 signal caution.

However, opportunities remain. A resurgent Chinese market, coupled with stabilization in Europe and the Middle East, could offset U.S. pain. If Swatch can accelerate its direct-to-consumer digital pivot and expand its certified pre-owned business, management may partially neutralize tariff headwinds. Savvy investors should conduct their own Swatch stock analysis 2025 using tools like the Fair Value Calculator at fairvalue-calculator.com to model best- and worst-case scenarios before committing capital.

Conclusion: Forecasting the Future of Swatch Amid Tariff Uncertainty

As Trump’s 39% tariffs loom large, Swatch faces a pivotal crossroads. The company’s strong brand and diversified portfolio offer some cushion, but price-sensitive markets and high valuation multiples heighten downside risk. Investors must remain vigilant, employing rigorous Swatch stock analysis 2025 to gauge emerging demand shifts and management’s strategic responses.

Ultimately, the coming quarters will reveal whether Swatch can adapt through market diversification and digital innovation or if tariff pressures will erode its once-unassailable position. For those seeking clarity, the Fair Value Calculator remains an invaluable resource to model potential outcomes and navigate this complex investment landscape.