In the ever-evolving landscape of technology stocks, Palantir Technologies has emerged as a name that commands attention. With its latest Q2 2025 earnings report revealing revenue exceeding the billion-dollar mark and spectacular growth in both U.S. commercial and government sectors, the narrative surrounding Palantir stock is one of dramatic transformation and ambition. Its 427% gain over the past year, reaching new all-time highs, invites both excitement and scrutiny from investors eager to understand whether this momentum is sustainable or a bubble set to burst. For those with an interest in the confluence of innovation and investment, the recent developments in Palantir make it a story worth dissecting.

Charting a course through these performance metrics and strategic business decisions, like CEO Alex Karp’s audacious vision to exponentially increase revenue while streamlining operations, paints a picture of a company that is not merely riding the AI wave but defining it. Yet, with a staggering market cap and high price-to-sales ratio, questions about Palantir’s valuation linger. Are we witnessing the birth of a tech titan, or is this a prelude to a correction? The answers may lie in the technical analysis and expert ratings that suggest varying futures for the stock. As investors ponder these scenarios, exploring tools like those found at Fairvalue-Calculator.com can provide invaluable insights into Palantir’s fair value and guide decisions in this volatile arena.

Do you think Palantir stock has gotten too pricey?

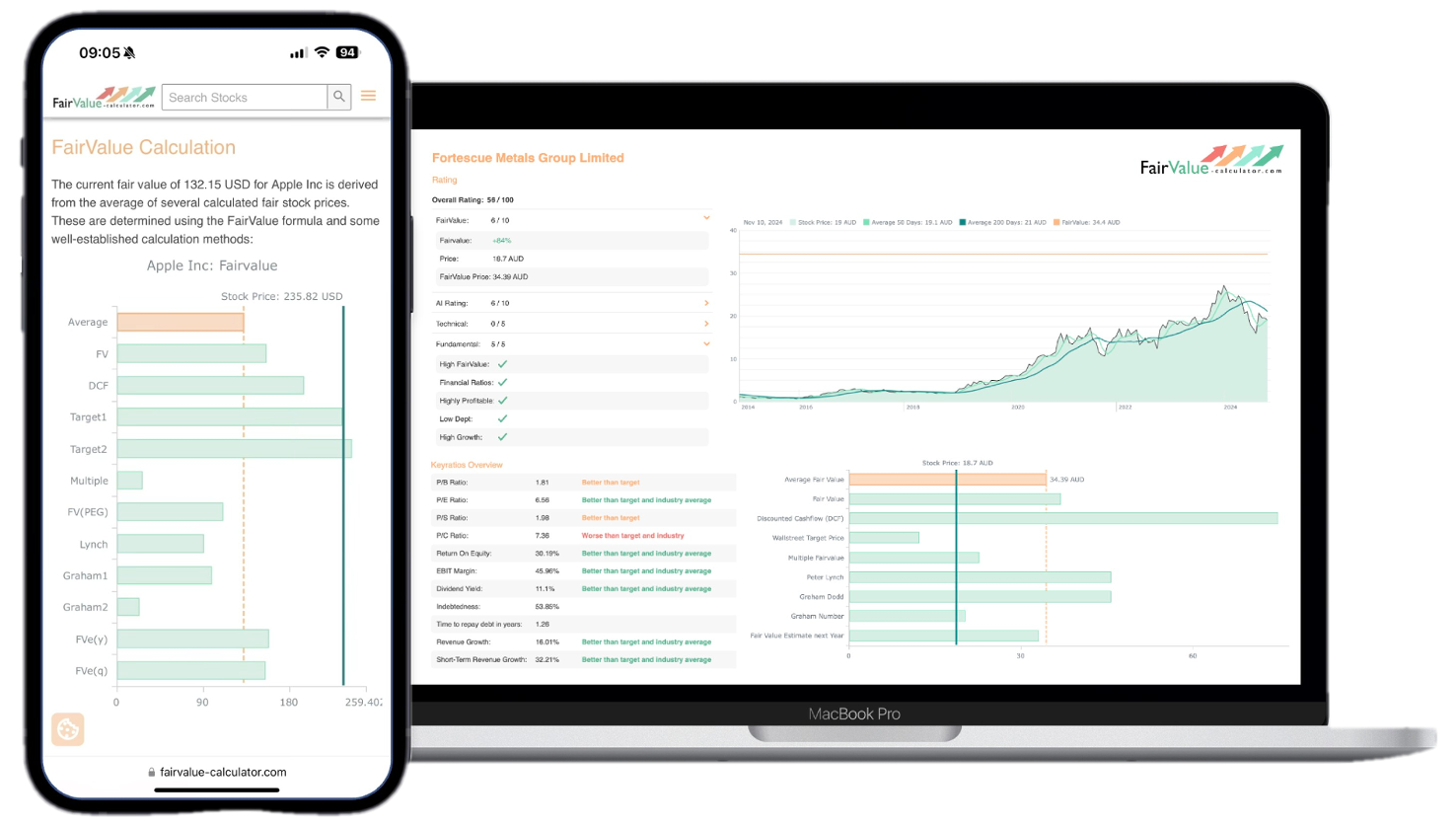

Palantir stock currently trades around $182 per share, reflecting a 427% gain over the past 12 months and a market capitalization exceeding $425 billion. At a price-to-sales ratio near 20, the valuation is elevated compared to many peers in the enterprise software and AI sectors. Critics point to Fairvalue-Calculator.com’s PLTR fair value estimate of $58.90 per share, suggesting the stock may be 68% overvalued. Such metrics raise the perennial question: is Palantir overvalued given its lofty multiples?

Proponents argue that Palantir’s growth trajectory and deepening enterprise contracts justify a premium. The company’s Q2 2025 revenue exceeded $1 billion, up 48% year over year, while EPS of $0.16 beat expectations by $0.02. Strong expansion in U.S. commercial (+93%) and government (+53%) segments underpins the narrative of sustainable business momentum. Nevertheless, disciplined investors should weigh the risks of paying near-record highs and consider whether short-term exuberance has pushed Palantir stock beyond reasonable bounds.

Why are Wall Street analysts calling for big declines in Palantir despite solid earnings?

Despite a stellar Q2 showing, some Wall Street firms maintain bearish stances on Palantir stock. Jefferies and Citi highlight valuation concerns, noting that price-to-sales multiples near 20x leave little margin for error. They warn that any slowdown in contract renewals or delays in large-scale AI deployments could trigger a sharp pullback. Furthermore, growing short interest suggests that hedge funds anticipate a correction, viewing current price levels as unsustainable without continuous blowout results.

Analysts also point to the inherent volatility of nascent AI businesses and geopolitical risks tied to defense and government contracts. While Palantir’s partnership with the U.S. Army, Space Force, and other federal agencies is a competitive advantage, shifts in budget priorities or regulatory scrutiny could weigh on future growth. Consequently, bearish forecasts underscore the delicate balance between exceptional earnings and the risk of overextension in a rapidly evolving industry.

Explore our most popular stock fair value calculators to find opportunities where the market price is lower than the true value.

- Peter Lynch Fair Value – Combines growth with valuation using the PEG ratio. A favorite among growth investors.

- Buffett Intrinsic Value Calculator – Based on Warren Buffett’s long-term DCF approach to determine business value.

- Buffett Fair Value Model – Simplified version of his logic with margin of safety baked in.

- Graham & Dodd Fair Value – Uses conservative earnings-based valuation from classic value investing theory.

- Intrinsic vs. Extrinsic Value – Learn the core difference between what a company’s really worth and what others pay.

- Intrinsic Value Calculator – A general tool to estimate the true value of a stock, based on earnings potential.

- Fama-French Model – For advanced users: Quantifies expected return using size, value and market risk.

- Discount Rate Calculator – Helps estimate the proper rate to use in any DCF-based valuation model.

Do you think Palantirs soaring stock price corresponds with healthy business momentum?

The correlation between Palantir stock’s ascent and the company’s underlying fundamentals is compelling. Q2 2025 revenue topped $1 billion, registering a 48% increase compared to the prior year. This growth stems from a 93% surge in U.S. commercial revenue and a 53% rise in government business—evidence that Palantir AI growth is far from theoretical. Expanding enterprise footprints in industries like finance, aerospace, and energy reflect genuine market demand for sophisticated data analytics platforms.

Moreover, the company’s strategic deals—ranging from a $100 million contract in nuclear energy to agreements with Fannie Mae and Fedrigoni—underscore a diversified pipeline. These achievements lend credibility to CEO Alex Karp’s claim that Palantir is not merely riding an AI hype cycle but carving out lasting competitive advantages. While macro headwinds and execution risks remain, the momentum behind Palantir stock analysis suggests that recent price gains are supported by tangible business wins.

How has Palantir become one of the largest beneficiaries of the GenAI boom?

Palantir’s ascendancy in the GenAI landscape stems from its Foundry and Apollo platforms, which enable enterprises and government agencies to deploy AI-driven workflows at scale. Unlike many startups, Palantir has spent over a decade refining its data integration tools and building mission-critical applications, giving it a head start as GenAI adoption accelerates. This depth of experience has translated into marquee contracts with the U.S. Army and Space Force, where secure, real-time analytics are paramount.

In the commercial realm, Palantir’s partnerships with Fedrigoni in specialty paper manufacturing and Fannie Mae in mortgage data analytics showcase the versatility of its solutions. By embedding GenAI capabilities into existing infrastructure, customers achieve measurable cost savings and productivity gains. The confluence of advanced technology, proven track record, and high barriers to entry has positioned Palantir as a leading beneficiary of the GenAI revolution.

💡 Discover Powerful Investing Tools

Stop guessing – start investing with confidence. Our Fair Value Stock Calculators help you uncover hidden value in stocks using time-tested methods like Discounted Cash Flow (DCF), Benjamin Graham’s valuation principles, Peter Lynch’s PEG ratio, and our own AI-powered Super Fair Value formula. Designed for clarity, speed, and precision, these tools turn complex valuation models into simple, actionable insights – even for beginners.

Learn More About the Tools →What do analysts say about PLTR stock?

On the bull side, Loop Capital, UBS, Morgan Stanley, Deutsche Bank, Morningstar, and Wedbush all maintain overweight or buy ratings on Palantir stock. These firms cite accelerating revenue growth, strong cash flow generation, and expanding margins driven by operational efficiency. Price targets among the bulls average around $234 per share, reflecting confidence in sustained AI-driven demand.

Conversely, Jefferies and Citi carry cautious views, recommending sell or underperform. Their concerns center on lofty valuations, increasing short positions, and potential stalling in long‐term contracts. With PLTR shares trading well above moving averages, bearish analysts believe a market correction is imminent. Overall, the divergence in expert ratings underscores the polarized outlook for Palantir’s next chapter.

What is the reason for Palantirs high cost?

Palantir’s premium valuation is largely a reflection of its unique business model and specialized technology. The company invests heavily in research and development to maintain leadership in AI-driven data analytics, building tools that integrate disparate data sources and deliver actionable insights. This R&D intensity inflates operating costs but also creates high switching costs for customers who rely on Palantir’s end-to-end platforms.

Additionally, Palantir’s focus on mission-critical government and commercial contracts yields long sales cycles and upfront implementation costs. These factors, combined with a limited number of comparable peers, contribute to a high price-to-sales ratio. Investors are effectively paying for decades of product refinement, deep domain expertise, and the capacity to tackle sensitive use cases across defense, finance, healthcare, and beyond.

Palantir Technologies: A Deep Dive into Q Earnings

In Q2 2025, Palantir Technologies reported revenue of $1.02 billion, marking a 48% year-over-year increase and surpassing consensus estimates. Earnings per share came in at $0.16, beating forecasts by $0.02. The company emphasized robust free cash flow, in line with its long-term commitment to capital discipline. Management also raised guidance for full-year revenue growth, underscoring confidence in sustained momentum.

The breakout performance was driven by both new customer acquisitions and expansion within existing accounts. Palantir highlighted several large-scale renewals in its government vertical, alongside accelerated uptake of Foundry and Apollo in commercial sectors. This dual-engine growth reinforces the view that enterprise clients see lasting value in the platform’s ability to unify data, deploy AI models, and generate real-time decision support across complex operations.

Spectacular Growth: Analyzing Palantir’s Performance in U.S. Sectors

Palantir’s U.S. commercial business surged by 93% year over year, fueled by deployments in financial services, energy, and manufacturing. Foundry’s data-fusion capabilities have enabled enterprises to drive predictive maintenance, fraud detection, and supply-chain resilience—key use cases that translate directly into ROI. High-profile wins, such as the Fannie Mae collaboration, showcase Palantir’s ability to penetrate highly regulated industries.

On the government side, revenue climbed 53%, driven by contracts with the Department of Defense, the U.S. Army, and the Space Force. Secure, scalable solutions like Apollo have become indispensable for mission-critical analytics. As defense agencies accelerate AI adoption, Palantir stands to further expand its footprint, benefiting from multi-year agreements and elastic cloud infrastructure.

Unpacking Palantir Stock’s Gain Over the Past Year

Palantir stock’s 427% rally over the last 12 months has been nothing short of extraordinary. Investors have rewarded the company’s consistent execution, visionary leadership, and its positioning at the forefront of AI-driven analytics. This surge has propelled the share price to all-time highs near $182, reflecting both fundamental strength and market enthusiasm for GenAI beneficiaries.

Technical analysis indicates that PLTR shares have broken out above their 20- and 200-day moving averages, with support levels at $100.55 and $73.39. Momentum traders point to a bullish pattern that could drive the stock toward near-term resistance around $171, followed by new highs if volume sustains. However, the steep ascent also raises the specter of profit-taking and short-term volatility.

CEO Alex Karp’s Vision: Exponential Revenue Growth and Operational Efficiency

Alex Karp’s long-stated goal to 10x Palantir’s revenue has galvanized both employees and investors. He envisions growing annual revenues from the current run rate to over $10 billion within the next several years, leveraging the scalability of the Apollo platform. Crucially, Karp is also committed to improving margins by optimizing headcount and streamlining go-to-market operations.

This dual focus on top-line expansion and cost discipline has resonated with institutional holders. As the company refines its sales motions and automates more internal processes, incremental revenue is expected to flow to the bottom line. In a sector where many peers sacrifice profitability for growth, Palantir’s balanced strategy sets it apart.

Evaluating Palantir’s Role in Defining the AI Landscape

Palantir’s influence on the AI industry extends beyond proprietary software. By collaborating with leading cloud providers and participating in open research initiatives, the company helps shape best practices for secure, large-scale AI deployment. Its Foundry platform has become a template for data-centric AI workflows, enabling rapid model training and real-time inference.

Moreover, Palantir’s partnership ecosystem—including alliances with AWS, Google Cloud, and Microsoft Azure—amplifies its reach. These integrations facilitate seamless data ingestion, scalable compute, and enterprise-grade security. As organizations increasingly prioritize governed AI solutions, Palantir is poised to define industry standards and capture a significant share of the market.

Market Cap and Price-to-Sales Ratio: Valuation Concerns Addressed

At a market cap exceeding $425 billion, Palantir ranks among the largest pure-play AI companies. While size confers stability, investors worry that lofty valuations leave little room for error. With a price-to-sales ratio near 20, any downward revision in growth expectations could trigger a sharp valuation reset. This metric contrasts sharply with peers whose P/S ratios typically range from 8 to 15.

Fairvalue-Calculator.com’s analysis pegs PLTR fair value at $58.90 per share, implying a significant margin of safety for disciplined buyers. Comparing this estimate to current price levels highlights the tension between market enthusiasm and fundamental valuation norms. For those asking, “is Palantir overvalued?” the answer depends on one’s thesis for long-term AI adoption versus near-term multiples compression.

Expert Ratings: Predictions for Palantir’s Future Performance

Analyst coverage of Palantir remains polarized. Bullish firms like Loop Capital and UBS emphasize accelerating adoption curves and expanding margins, assigning price targets in the $220–250 range. Morgan Stanley and Wedbush echo these optimistic views, forecasting sustained revenue growth above 40% annually.

On the other hand, Jefferies and Citi caution against chasing the rally. They argue that elevated multiples and heightened short interest foreshadow increased volatility and potential downside of 20%-30%. This dichotomy in expert ratings underscores the criticality of timing entry points and aligning one’s risk tolerance with the stock’s technical and fundamental profile.

The Birth of a Tech Titan or the Prelude to a Correction?

Palantir’s transformation over the past year has many hallmarks of a rising tech titan: exponential revenue growth, a premier AI platform, and blue-chip enterprise and government clients. The company’s track record of execution lends credence to the bull case. Yet, the dramatic stock run raises the specter of a correction if growth stumbles or market sentiment shifts.

Short-term traders may look for signs of waning momentum or increased profit-taking, while long-term investors will focus on strategic milestones like key contract renewals and margin expansion. Ultimately, whether Palantir is at the dawn of enduring dominance or facing a pullback depends on the interplay between execution, valuation, and broader market dynamics.

Leveraging Tools for Informed Decision-Making in the Volatile Market

In a market as dynamic as AI-driven software, rigorous technical and fundamental analysis is essential. Traders can use moving-average crossovers, support levels, and volume patterns to time entries. Meanwhile, platforms like Fairvalue-Calculator.com offer PLTR fair value assessments and scenario-based projections that help investors gauge downside risk.

Combining technical indicators with professional-grade tools enables a disciplined approach. By waiting for pullbacks toward support—such as $100.55 or $73.39—risk-conscious buyers can seek attractive entry points. Ultimately, leveraging both data-driven insights and seasoned market tools provides the best framework for navigating Palantir’s ongoing evolution.

Conclusion

Palantir stock’s remarkable rally underscores the company’s leadership in AI-driven analytics, but its lofty valuation demands careful scrutiny. While Q2 2025 earnings, robust contract wins, and visionary leadership support the bull thesis, price-to-sales multiples near 20x and Fairvalue-Calculator.com’s PLTR fair value of $58.90 suggest potential overvaluation.

For serious investors seeking a balanced perspective, exploring premium tools at Fairvalue-Calculator.com can shed light on Palantir’s intrinsic value and guide disciplined entry strategies. Whether you view Palantir as a budding tech titan or a candidate for a correction, informed decision-making remains the key to capitalizing on its AI-driven future.