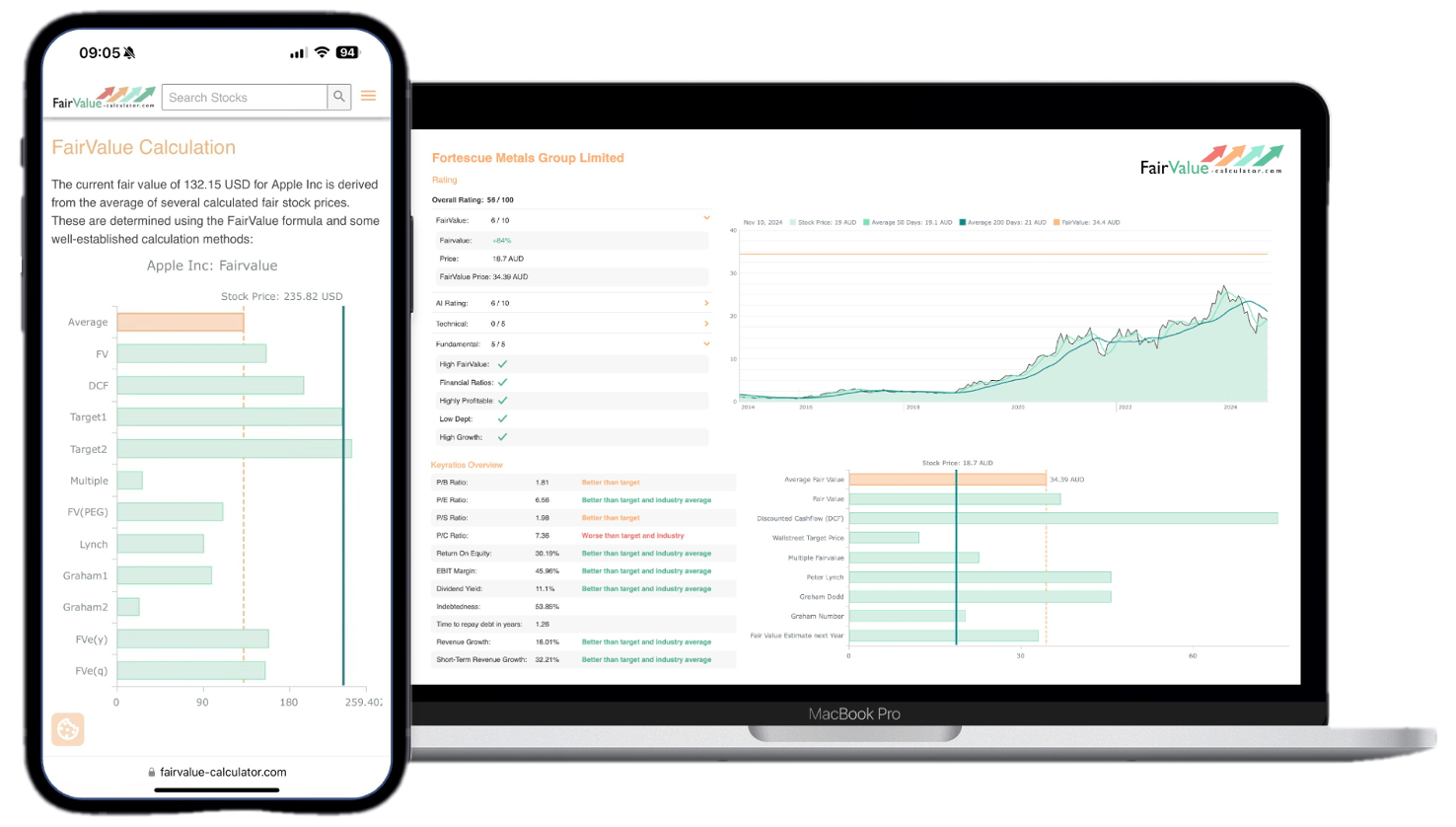

In the labyrinth of financial statements and accounting standards, “fair value” often emerges as a beacon of both clarity and confusion. While this concept is pivotal for accurate financial reporting, it frequently leaves professionals juggling between definitions under IFRS and GAAP frameworks. But what does “fair value” mean in accounting or IFRS / GAAP, really? Understanding this can be the key to unlocking more transparent financial insights and decisions. As you embark on this journey, consider the role of reliable tools like fairvalue-calculator.com, which aids in simplifying this complex landscape by helping evaluate stock valuations with precision.

Imagine navigating through a sea of numbers where each figure tells its own story about a company’s worth. Fair value, in essence, seeks to capture these narratives by providing a realistic assessment of an asset’s market value. This blog post aims to demystify the intricacies surrounding fair value measurements under different accounting standards. Whether you’re an accountant trying to reconcile differing methodologies, or an investor seeking clearer insights into a company’s valuation, understanding fair value is essential. Dive in to unravel these complexities and equip yourself with knowledge that brings accuracy and transparency to light.

Understanding the Concept of Fair Value in Accounting

Fair value sits at the intersection of market dynamics, investor expectations, and financial reporting. At its core, it represents the price at which an asset could be exchanged or a liability settled between knowledgeable, willing parties in an arm’s-length transaction. It is distinct from historical cost, which records the actual price paid for an asset when it was acquired. Instead, fair value emphasizes a current market-based measurement, capturing real-time fluctuations in supply and demand.

When we ask, “What does ‘fair value’ mean in accounting or IFRS / GAAP?” we’re probing how standards define, measure, and disclose this metric. Under both IFRS and GAAP, fair value aims to present users of financial statements with transparent insights into an organization’s financial health. Yet, the approaches can diverge on key points, such as valuation techniques and disclosure requirements. Grasping the foundational concept of fair value is a stepping stone to navigating the more nuanced differences across standards, which we will explore in later sections.

Importance of Fair Value in Financial Reporting

The adoption of fair value accounting marks a significant shift toward relevance and timeliness in financial reporting. Traditional cost-based models may obscure the true economic value of an entity’s assets and liabilities, especially during periods of volatility. Fair value, by contrast, strives to provide stakeholders with information that better reflects current market conditions, thereby enhancing decision usefulness for investors, creditors, and regulators.

Transparency is a cornerstone of modern financial markets. When companies measure assets like investment securities, derivatives, or real estate at fair value, they communicate more accurate risk exposures and potential upside to stakeholders. This improved clarity can influence credit ratings, investment flows, and strategic planning. Furthermore, fair value assessments can impact income statement volatility, recognizing unrealized gains and losses, but many argue this volatility conveys meaningful information about a company’s true financial position. Ultimately, embracing fair value fosters trust in financial statements by aligning reported figures more closely with underlying economic realities.

Variations in Fair Value Measurement under IFRS and GAAP

Although IFRS and US GAAP both define fair value as a market-based measurement, subtle distinctions emerge in application. IFRS 13 prescribes a robust framework centered on an exit-price notion, focusing on the price to sell an asset. GAAP’s Guidance under ASC 820, while similar in spirit, traditionally emphasizes an entrance price or transaction price for acquiring an asset or assuming a liability.

Differences can manifest in valuation techniques, hierarchy levels for inputs, and disclosure requirements. For instance, IFRS requires enhanced disclosures around unobservable inputs and sensitivity analyses. GAAP, meanwhile, has historically afforded more industry-specific guidance, which can yield divergent practices in certain sectors. We’ll delve deeper into these nuances in the sections on principles and comparison further below.

Explore our most popular stock fair value calculators to find opportunities where the market price is lower than the true value.

- Peter Lynch Fair Value – Combines growth with valuation using the PEG ratio. A favorite among growth investors.

- Buffett Intrinsic Value Calculator – Based on Warren Buffett’s long-term DCF approach to determine business value.

- Buffett Fair Value Model – Simplified version of his logic with margin of safety baked in.

- Graham & Dodd Fair Value – Uses conservative earnings-based valuation from classic value investing theory.

- Intrinsic vs. Extrinsic Value – Learn the core difference between what a company’s really worth and what others pay.

- Intrinsic Value Calculator – A general tool to estimate the true value of a stock, based on earnings potential.

- Fama-French Model – For advanced users: Quantifies expected return using size, value and market risk.

- Discount Rate Calculator – Helps estimate the proper rate to use in any DCF-based valuation model.

Key Principles of Fair Value Accounting

Fair value accounting is anchored on three overarching principles: a market-based measurement, an exit price perspective, and a fair value hierarchy. First, a market-based measurement presumes that independent market participants transact at prevailing prices for similar or identical assets. Second, the exit price concept underscores a seller’s view, focusing on the price received to sell an asset rather than the cost to acquire it.

The fair value hierarchy categorizes inputs into three levels, Level 1 (quoted prices in active markets), Level 2 (observable inputs other than quoted prices), and Level 3 (unobservable inputs like management assumptions). This tri-level structure ensures users can gauge the reliability and subjectivity embedded in each valuation. Adhering to these principles promotes consistency, comparability, and transparency in financial statements, regardless of regional accounting frameworks.

Challenges Faced in Determining Fair Value

Measuring fair value may seem straightforward in active, liquid markets, but real-world conditions often present obstacles. Thin trading volumes, lack of comparable transactions, and rapidly changing economic factors can compromise the availability of reliable market data. When observable inputs are scarce, companies must resort to Level 3 valuations, which rely heavily on internal models and assumptions.

Subjectivity pervades these estimates. Management judgments on discount rates, cash flow projections, and risk adjustments can materially influence reported fair values. Auditors and regulators commonly challenge these valuations, requesting extensive documentation and stress testing. Moreover, fair value volatility can introduce earnings swings, unsettling investors and increasing scrutiny on quarterly performance. Balancing relevance with reliability remains an ongoing challenge in fair value measurement.

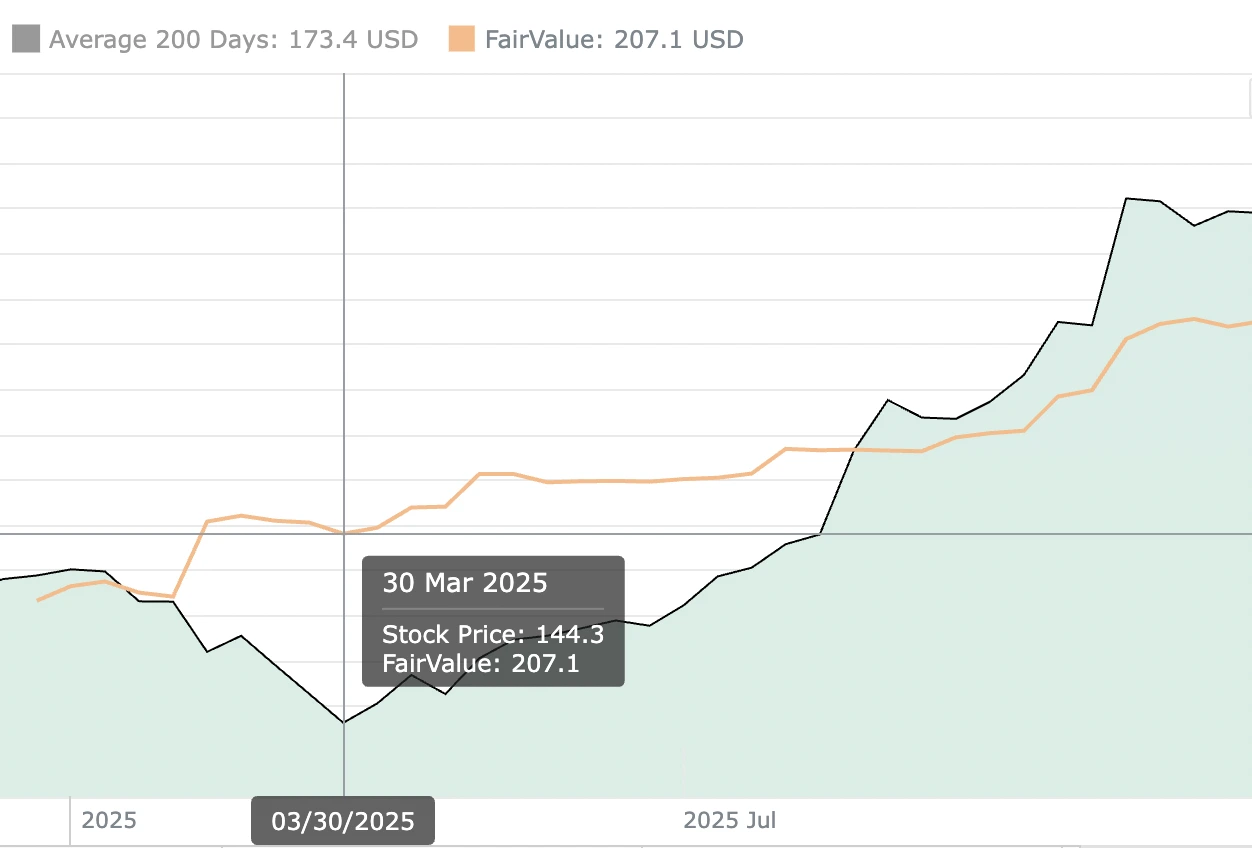

💡 Discover Powerful Investing Tools

Stop guessing – start investing with confidence. Our Fair Value Stock Calculators help you uncover hidden value in stocks using time-tested methods like Discounted Cash Flow (DCF), Benjamin Graham’s valuation principles, Peter Lynch’s PEG ratio, and our own AI-powered Super Fair Value formula. Designed for clarity, speed, and precision, these tools turn complex valuation models into simple, actionable insights – even for beginners.

Learn More About the Tools →Impact of Fair Value on Financial Statements

Recognizing fair value can reshape a company’s balance sheet and income statement. Assets measured at fair value may rise or fall with market conditions, directly affecting equity through other comprehensive income or net income, depending on classification. Liabilities marked to fair value, such as derivatives or contingent liabilities, also fluctuate, potentially altering leverage ratios and debt covenants.

Investors and analysts pay close attention to these movements. Unrealized gains could bolster equity, but they might also signal elevated risk if valuations rely on unobservable inputs. Conversely, fair value impairments can erode profitability and trigger off-balance sheet disclosures. Ultimately, the dynamic nature of fair value means stakeholders must scrutinize valuation methodologies, underlying assumptions, and the persistence of recognized gains or losses over time.

Fair Value Calculation Methods

Three primary valuation techniques underpin fair value measurement: the market approach, income approach, and cost approach. The market approach uses prices and other relevant information from market transactions involving identical or comparable assets. The income approach discounts expected future cash flows or employs capitalization rates to derive present value.

The cost approach, sometimes called the replacement cost method, estimates the amount required to replace an asset’s service capacity. Each method has strengths and limitations: the market approach excels in active markets, the income approach suits intangible or unique assets, and the cost approach applies when neither market nor income data are available. Selecting the appropriate method hinges on the asset’s nature, data availability, and the fair value hierarchy level.

Comparing Fair Value under IFRS and GAAP

While IFRS 13 and ASC 820 share the same objective, their handling of fair value contains nuances. IFRS prioritizes an exit price notion and requires extensive disclosures, including sensitivity analyses for Level 3 inputs. GAAP’s guidance, though aligned in essence, traditionally offered more industry-specific practical expedients.

For example, under IFRS, investment property can be measured at fair value with changes recognized in profit or loss, whereas GAAP often uses historical cost with impairment testing. Additionally, the two frameworks diverge on measurement of certain nonfinancial liabilities, such as decommissioning obligations. Understanding these subtleties is vital for companies operating across borders, ensuring consistency in reporting and avoiding reconciliation discrepancies.

Applications of Fair Value in Different Industries

Various industries leverage fair value in distinct ways. Financial services firms frequently mark securities and derivatives to market, using Level 1 and Level 2 inputs. Real estate enterprises may invest in valuation reports and active market data to support Level 3 estimates. Technology companies rely on the income approach to value intangible assets like patents and trademarks, projecting future cash flows.

Commodity producers use fair value to reflect inventory measured on a net realizable value basis, capturing price swings in raw materials. Even the energy sector employs complex models for decommissioning liabilities and power purchase agreements. Regardless of industry, the core principles remain constant: fair value enhances transparency, but demands rigorous documentation, robust controls, and continuous reassessment.

Conclusion: Enhancing Financial Clarity Through Fair Value Analysis

Fair value stands as a cornerstone of modern accounting, bridging the gap between financial statements and actual market dynamics. By embracing a market-based measurement, companies offer stakeholders timely insights into asset performance, risk exposures, and potential earnings volatility. Although IFRS and GAAP exhibit subtle differences in application and disclosure requirements, their shared objective underscores the universal value of transparency.

From financial services to manufacturing, fair value plays a pivotal role in shaping investment decisions and regulatory oversight. Leveraging tools like fairvalue-calculator.com for stock valuation can streamline this complex process, providing reliable inputs and enhancing consistency. Armed with a deep understanding of fair value principles and methodologies, professionals can drive greater clarity, and confidence, in the numbers that matter most.