In the dynamic world of finance, understanding the intricacies of value can make all the difference between a solid investment and a regrettable loss. But how does one navigate the seemingly complex terrain of estimating a company’s worth? Enter the concept of fair value estimates, a vital tool for investors, analysts, and financial professionals alike. By diving into this topic, we uncover not just numbers, but the story behind them, an analytical narrative that can illuminate the true potential and risks of an investment. If you’re seeking clarity amidst the financial fog, you’re about to embark on an enlightening journey.

Imagine standing at a crossroads where each path represents a different valuation of the same asset. This scenario illustrates the range of fair value estimates, a spectrum where numbers are shaped by varying methodologies, market conditions, and economic assumptions. In this blog post, we’ll delve into the heart of these estimates, uncovering how they are determined and the extent to which they can influence decision-making in the investment landscape. Whether you’re a seasoned investor or a curious newcomer, understanding what is the range of fair value estimates is crucial for making informed and strategic financial decisions.

Exploring the Concept of Fair Value Estimates

Fair value estimates represent an informed approximation of an asset’s intrinsic worth, grounded in current market data, company-specific information, and broader economic indicators. Unlike book value or historical cost, fair value seeks to capture what a buyer would rationally pay for an asset in an arm’s-length transaction. This concept directly addresses the inherent dynamism of markets, where prices fluctuate daily based on new information and shifting investor sentiment.

At its core, fair value estimation involves synthesizing qualitative insights—such as brand strength, management quality, and competitive positioning—with quantitative metrics like discounted cash flow projections or comparable company multiples. Because no single metric can perfectly capture every nuance of an asset’s prospective performance, practitioners often produce a range of fair value estimates rather than a solitary point estimate. This spectrum reflects varying assumptions about growth rates, discount rates, and risk premiums, illuminating the degree of confidence or uncertainty surrounding each valuation.

Importance of Fair Value Estimates in Finance

Fair value estimates serve as a cornerstone for modern financial analysis, providing investors, analysts, and corporate managers with a transparent benchmark against which to measure market prices. Regulatory frameworks such as IFRS 13 and FASB’s ASC 820 mandate the use of fair value for financial reporting, ensuring consistency and comparability of balance sheets and performance disclosures. By aligning book values more closely with market realities, these guidelines help stakeholders assess an entity’s true financial health.

Beyond compliance, fair value estimates influence a wide array of strategic decisions. Investment committees rely on valuations to determine entry and exit points, while corporate development teams use them to evaluate merger and acquisition targets. Lenders reference fair value calculations when setting collateral requirements, and auditors scrutinize them to confirm that asset impairments or revaluations are justified. In each case, accurate fair value estimates reduce information asymmetry, lower transaction costs, and enhance market efficiency.

Factors Influencing Fair Value Estimates

Multiple variables converge to shape a fair value estimate. Company-specific factors such as revenue growth prospects, profit margins, and capital structure determine underlying cash flows. Simultaneously, industry dynamics, competitive intensity, regulatory changes, and technological disruption, introduce additional layers of risk or opportunity that must be quantified.

Beyond these internal and sectoral considerations, macroeconomic elements like interest rates, inflation expectations, and currency fluctuations play a critical role. A rising interest rate environment, for instance, raises discount rates and tends to lower present valuations, while low-inflation periods can bolster fair value by reducing required returns. Understanding how each factor interrelates is vital for constructing robust valuation models that reflect the real-world context.

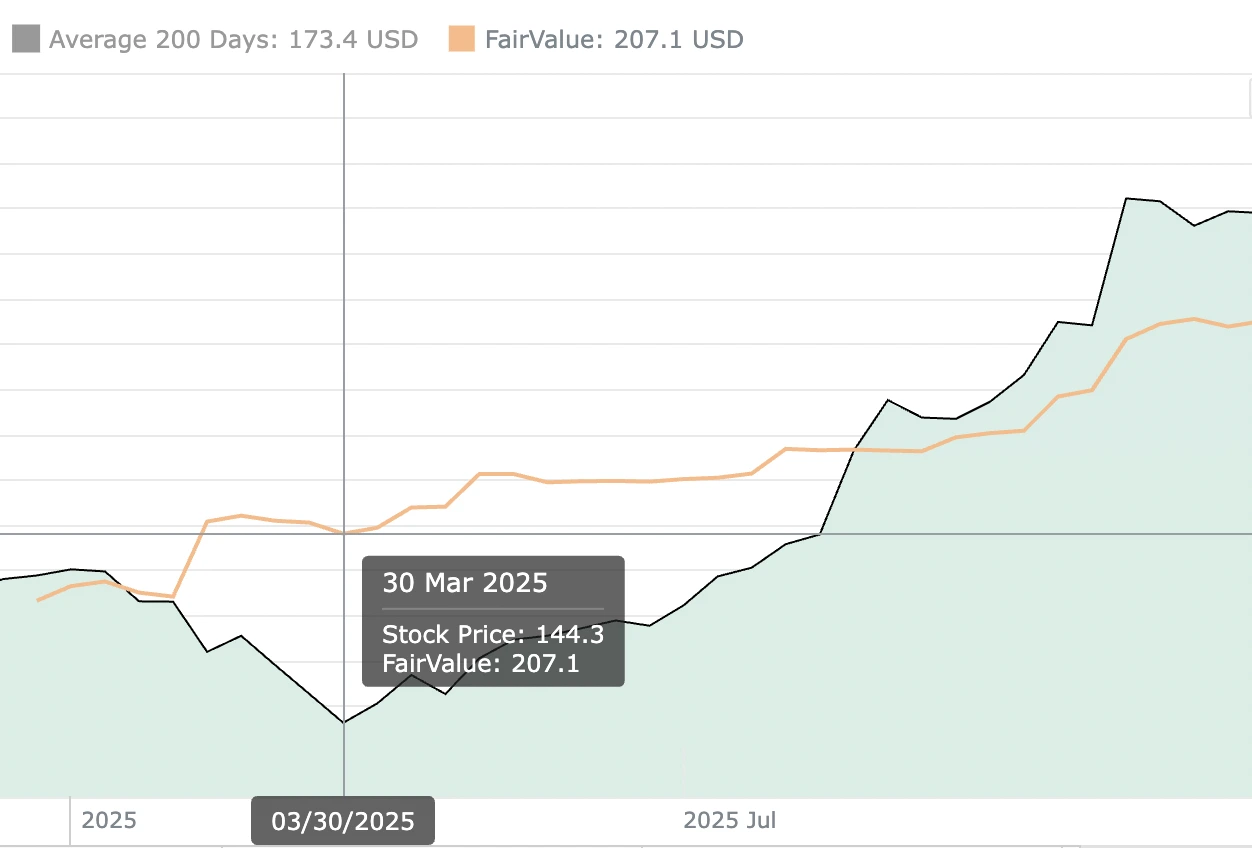

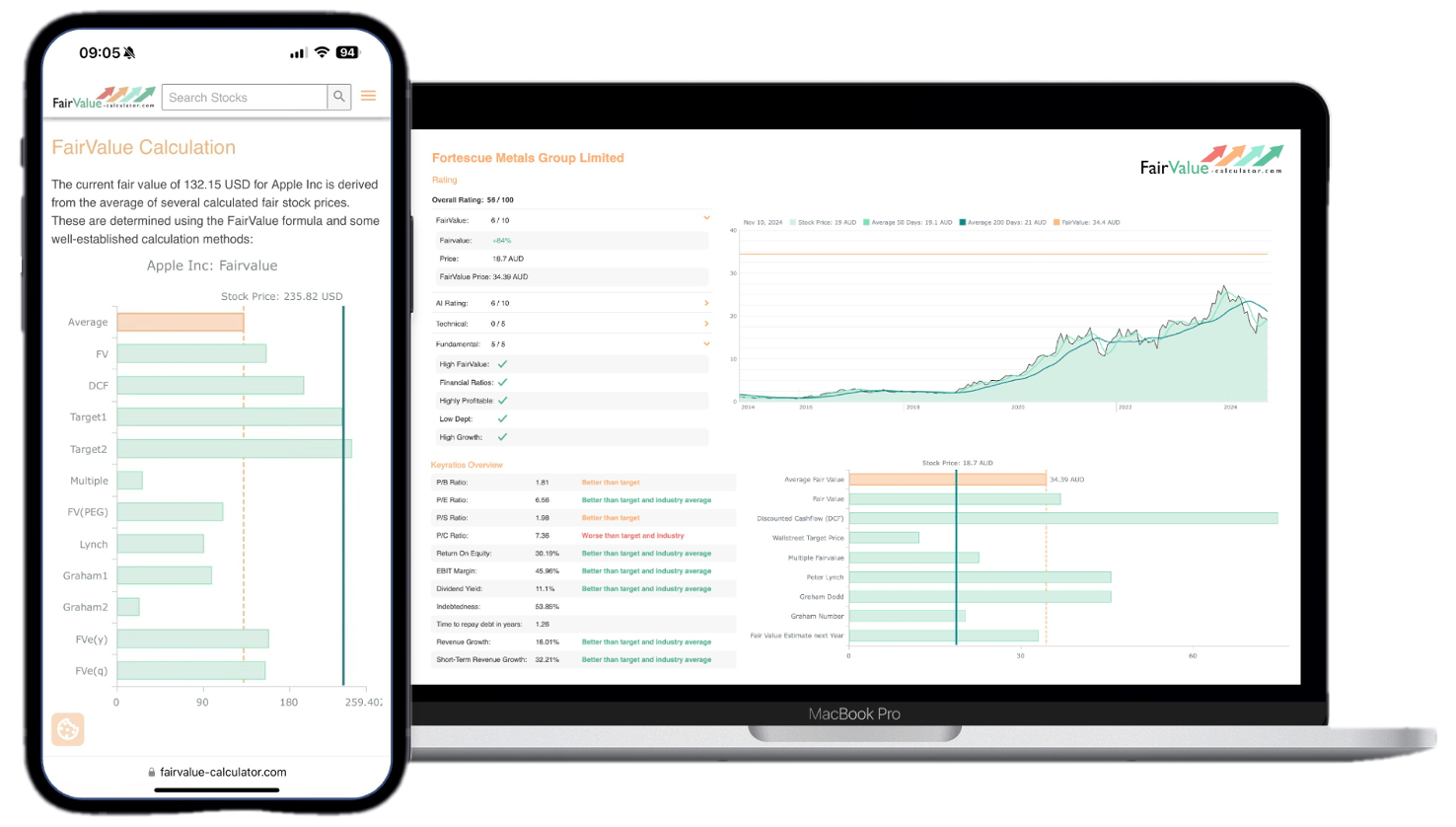

Explore our most popular stock fair value calculators to find opportunities where the market price is lower than the true value.

- Peter Lynch Fair Value – Combines growth with valuation using the PEG ratio. A favorite among growth investors.

- Buffett Intrinsic Value Calculator – Based on Warren Buffett’s long-term DCF approach to determine business value.

- Buffett Fair Value Model – Simplified version of his logic with margin of safety baked in.

- Graham & Dodd Fair Value – Uses conservative earnings-based valuation from classic value investing theory.

- Intrinsic vs. Extrinsic Value – Learn the core difference between what a company’s really worth and what others pay.

- Intrinsic Value Calculator – A general tool to estimate the true value of a stock, based on earnings potential.

- Fama-French Model – For advanced users: Quantifies expected return using size, value and market risk.

- Discount Rate Calculator – Helps estimate the proper rate to use in any DCF-based valuation model.

Common Methodologies for Determining Fair Value

Valuation practitioners frequently turn to three primary methodologies: the Discounted Cash Flow (DCF) approach, Comparable Company Analysis (CCA), and Precedent Transaction Analysis (PTA). Each method varies in data requirements, computational complexity, and sensitivity to assumptions.

In a DCF model, future free cash flows are forecasted and discounted back to present value using an appropriate discount rate, typically the weighted average cost of capital. Comparable Company Analysis, by contrast, benchmarks valuation multiples—such as EV/EBITDA or P/E, of peer firms to derive a relative fair value. Precedent Transaction Analysis assesses prices paid in historical M&A deals within the same industry, adjusting for deal specifics and time frame. Employing multiple methodologies and triangulating results often yields the most balanced estimate.

The Role of Market Conditions in Fair Value Estimation

Market sentiment and liquidity profoundly affect fair value estimates. A highly liquid market with active trading allows for more reliable price discovery, whereas thinly traded assets can exhibit wide bid-ask spreads that complicate valuation. Bull markets tend to inflate asset prices, often leading to optimistic fair value projections, while bear markets exert downward pressure and provoke conservative estimates.

Volatility measures, such as implied volatility from options markets or historical price swings, also inform risk premiums. Higher volatility translates into a larger discount rate or required rate of return, reducing present valuations. Therefore, analysts must continuously monitor market indicators to update fair value estimates in real time, ensuring they remain aligned with prevailing conditions.

💡 Discover Powerful Investing Tools

Stop guessing – start investing with confidence. Our Fair Value Stock Calculators help you uncover hidden value in stocks using time-tested methods like Discounted Cash Flow (DCF), Benjamin Graham’s valuation principles, Peter Lynch’s PEG ratio, and our own AI-powered Super Fair Value formula. Designed for clarity, speed, and precision, these tools turn complex valuation models into simple, actionable insights – even for beginners.

Learn More About the Tools →Understanding Economic Assumptions in Fair Value Estimates

Economic assumptions underpin every valuation model, serving as the foundation for cash flow projections, discount rates, and terminal value calculations. Key assumptions include projected GDP growth, sector-specific demand trends, and inflation rates. These macroeconomic variables directly influence revenue forecasts and cost structures, shaping the trajectory of future cash flows.

Discount rates incorporate additional assumptions about the risk-free rate (often based on government bond yields), equity risk premiums, and specific company risk factors. Small deviations in these inputs can lead to significant swings in fair value estimates, underscoring the importance of rigorous scenario analysis. Sensitivity testing—adjusting one assumption at a time, helps analysts gauge how vulnerable their valuations are to changes in economic outlooks.

Impact of Fair Value Estimates on Investment Decision-Making

Investors rely on fair value estimates to identify undervalued or overvalued opportunities. If the prevailing market price is substantially below the estimated fair value, the asset may present a buying opportunity, offering potential upside as the market corrects. Conversely, when market prices exceed fair value estimates, the risk of a price correction increases, signaling caution or potential profit-taking for existing long positions.

Portfolio managers also use fair value ranges to allocate capital more efficiently. By weighting investments based on the magnitude of deviation from fair value, they can optimize risk-adjusted returns. In addition, hedge funds and long-short strategies often construct pairs trades by going long on assets trading at a discount to their fair value and shorting those at a premium, aiming to profit from convergence over time.

Interpreting the Range of Fair Value Estimates

When investors ask, “What is the range of fair value estimates?” they’re seeking clarity on how different assumptions and methodologies impact valuation outcomes. Rather than presenting a single point estimate, analysts often produce a low, base, and high scenario to capture best-case, most-likely, and worst-case possibilities.

Interpreting this range involves assessing which inputs drive the widest dispersion. For example, variations in long-term growth rates or terminal multiples can widen the upper and lower bounds significantly. A narrow range suggests strong consensus among methodologies and assumptions, indicating higher confidence in the valuation. A broad range, by contrast, highlights elevated uncertainty, cautioning investors to factor in potential downside risks or upside volatility before committing capital.

Practical Applications of Fair Value Estimates

Fair value estimates find application across numerous financial activities. Corporate finance teams use them for strategic planning, budgeting, and evaluating capital investments. When considering a new project, companies compare the project’s net present value against its cost to determine economic viability. This ensures resources are allocated to initiatives with the highest potential returns.

In mergers and acquisitions, fair value estimates guide negotiation tactics and deal structuring. Acquirers base their offers on estimated synergies and standalone valuations, while targets leverage these figures to justify their asking price. In the accounting realm, fair value estimates are crucial for impairment testing of goodwill and financial assets, ensuring that balance sheet values remain reflective of current market realities.

Conclusion: Navigating the Complexities of Fair Value Estimation

Navigating fair value estimation demands a balanced fusion of quantitative rigor and qualitative judgment. By understanding the key drivers, market conditions, economic assumptions, and methodological choices, financial professionals can produce robust value ranges that inform strategic decision-making.

While no single estimate can capture every market twist, embracing the range of fair value estimates equips investors with a nuanced perspective. Ultimately, this approach enhances transparency, reduces risk, and fosters more disciplined investment practices.