In today’s rapidly evolving financial landscape, understanding the true worth of an asset is more crucial than ever. The art of fair value assessment has emerged as a beacon for investors, guiding them through the often murky waters of financial decision-making. This powerful tool does not just offer a snapshot of an asset’s potential market value; it provides a comprehensive picture that can influence investment strategies, risk management, and even corporate governance. For anyone navigating the complex world of finance, unlocking the insights offered by fair value assessment can be the difference between seizing profitable opportunities and missing out on critical trends.

Imagine you’re an investor deciding where to place your hard-earned money. Traditional valuation methods might have you relying on historical costs or book values, potentially painting an incomplete picture. However, fair value assessment brings to light the present market conditions, offering a real-time, transparent view of an asset’s worth. Whether you’re a seasoned financier or a newcomer looking to make informed choices, understanding the nuances of fair value can arm you with the insights you need to maximize returns and mitigate risks effectively. This blog post delves into the transformative power of fair value assessment, exploring how it can redefine your approach to investing and financial analysis.

The Importance of Fair Value Assessment in Modern Finance

In today’s global markets, determining an asset’s true worth is more than a bookkeeping exercise—it’s a strategic imperative. Fair value assessment goes beyond simple historical cost accounting to capture what an asset could fetch in the current market. Investors, analysts, and corporate leaders increasingly rely on this dynamic measure to make critical decisions, from mergers and acquisitions to asset disposals and funding rounds. By reflecting prevailing economic conditions, interest rates, and market sentiment, fair value assessment ensures that financial statements remain relevant and informative, reducing the risk of mispricing and misguided strategies.

Moreover, regulatory bodies and standard setters, such as the International Accounting Standards Board (IASB) and the Financial Accounting Standards Board (FASB), have emphasized fair value assessment in recent years. Their guidance underscores transparency and comparability, which help stakeholders evaluate performance consistently across industries and borders. As fair value metrics become more deeply embedded in reporting frameworks, companies that embrace rigorous assessment methodologies can build greater investor confidence, lower capital costs, and enhance their overall market reputation.

Differences Between Fair Value and Historical Cost Accounting

While both fair value assessment and historical cost accounting aim to quantify asset value, they diverge fundamentally in approach and outcome. Historical cost records an asset’s purchase price and carries it forward, less depreciation or impairment, regardless of market changes. It offers simplicity and objectivity, as values are verifiable and based on past transactions. However, this method may obscure economic realities when market conditions shift dramatically.

By contrast, fair value accounting revalues assets and liabilities at each reporting date, reflecting what they would command in an active market exchange. This dynamic remeasurement can lead to more volatile earnings but delivers timely insights. Investors gain a clearer view of an entity’s current financial position, allowing for more informed decisions. Nevertheless, the subjectivity involved in estimating fair values—especially for illiquid or unique assets—poses challenges that require robust governance and expert judgment.

Key Principles of Fair Value Assessment

At the core of fair value assessment are a few guiding principles designed to ensure consistency and transparency. First, the “exit price” concept focuses on what a market participant would pay to acquire or transfer an asset, rather than replacement cost. Second, the “highest and best use” principle considers the optimal way an asset could be deployed to maximize value. Finally, the hierarchical approach to inputs—Level 1, Level 2, and Level 3—ranks data quality from observable market prices to unobservable estimates.

Implementing these principles requires careful application of judgment and documentation. Valuers must analyze market activity, comparable transactions, and model assumptions while disclosing key inputs and methods. Through adherence to these core tenets, fair value assessment achieves its goal of providing users with reliable, decision-useful information that reflects current economic conditions rather than historical transactions alone.

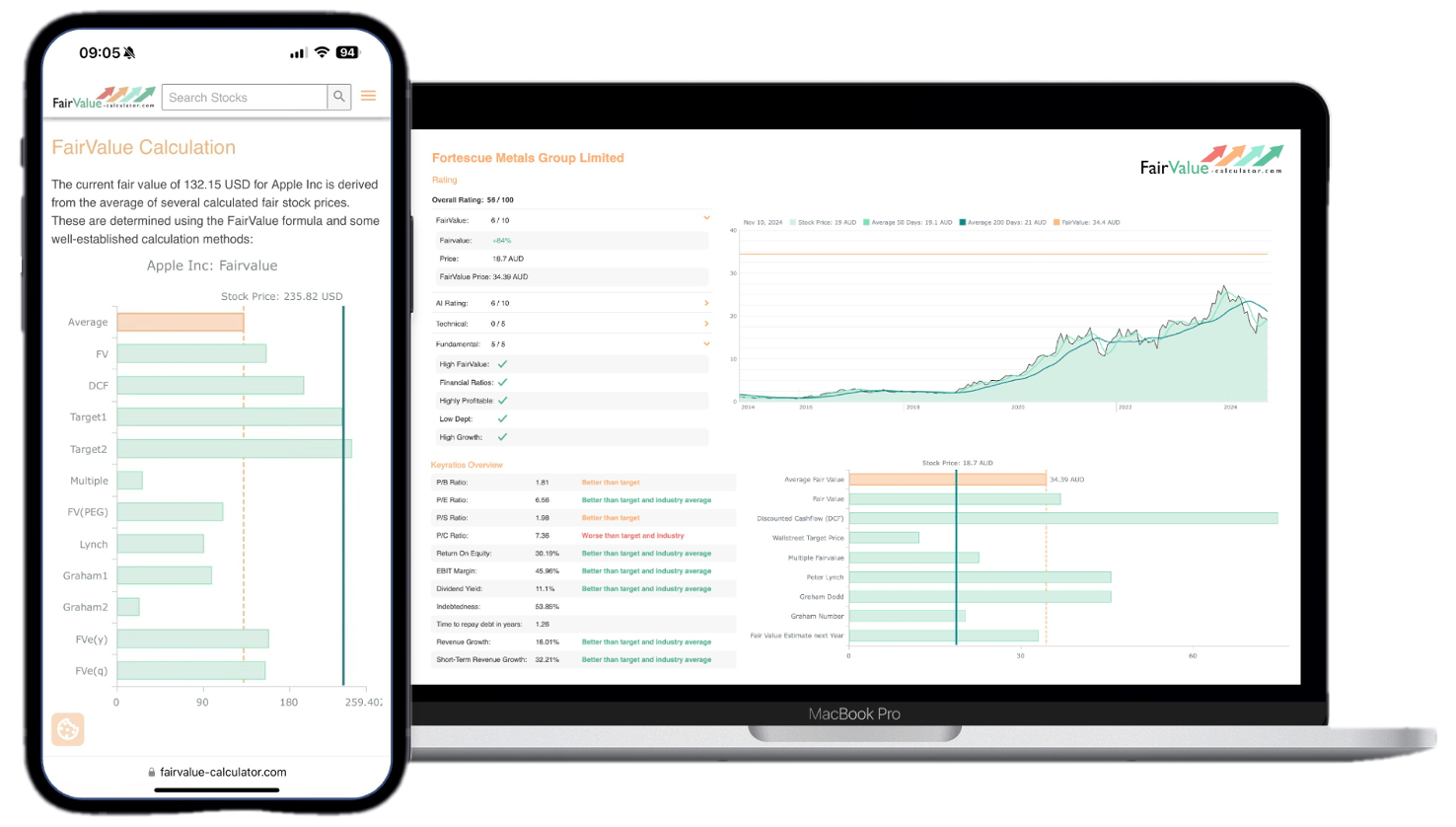

Explore our most popular stock fair value calculators to find opportunities where the market price is lower than the true value.

- Peter Lynch Fair Value – Combines growth with valuation using the PEG ratio. A favorite among growth investors.

- Buffett Intrinsic Value Calculator – Based on Warren Buffett’s long-term DCF approach to determine business value.

- Buffett Fair Value Model – Simplified version of his logic with margin of safety baked in.

- Graham & Dodd Fair Value – Uses conservative earnings-based valuation from classic value investing theory.

- Intrinsic vs. Extrinsic Value – Learn the core difference between what a company’s really worth and what others pay.

- Intrinsic Value Calculator – A general tool to estimate the true value of a stock, based on earnings potential.

- Fama-French Model – For advanced users: Quantifies expected return using size, value and market risk.

- Discount Rate Calculator – Helps estimate the proper rate to use in any DCF-based valuation model.

Techniques for Implementing Fair Value Measurement

Organizations can adopt various measurement techniques to perform fair value assessment, depending on asset type and market depth. Three primary approaches—market, income, and cost—each have distinct applications. The market approach uses observable transaction prices for identical or similar assets. The income approach derives value from projected cash flows, discounted to present value. The cost approach estimates replacement cost, adjusted for obsolescence.

Choosing the right method hinges on data availability and asset characteristics. For actively traded securities, market prices (Level 1 inputs) offer the most straightforward path. For specialized machinery or intellectual property, valuers may rely on income-based models (Level 3 inputs), requiring rigorous assumptions about future performance. Regardless of technique, transparency in methodology and sensitivity analyses strengthens the reliability of the fair value assessment.

Impact of Fair Value Assessment on Investment Strategies

Investors harness fair value assessment to pinpoint undervalued or overvalued assets relative to market consensus. By comparing an asset’s fair value estimate to its current trading price, portfolio managers can generate buy or sell signals. This discipline fosters disciplined entry and exit strategies, potentially enhancing long-term returns. Additionally, fair value metrics support benchmarking against peers and industry norms, enabling more granular performance attribution.

Beyond security selection, fair value assessment informs asset allocation decisions. In periods of heightened volatility, revaluations can highlight shifts in risk premia and liquidity, guiding tactical adjustments. Hedge funds and quantitative strategies, in particular, embed fair value signals into algorithmic models. Even pension funds and insurers leverage these insights to align liabilities with asset portfolios, aiming for regulatory compliance and stable funding ratios.

💡 Discover Powerful Investing Tools

Stop guessing – start investing with confidence. Our Fair Value Stock Calculators help you uncover hidden value in stocks using time-tested methods like Discounted Cash Flow (DCF), Benjamin Graham’s valuation principles, Peter Lynch’s PEG ratio, and our own AI-powered Super Fair Value formula. Designed for clarity, speed, and precision, these tools turn complex valuation models into simple, actionable insights – even for beginners.

Learn More About the Tools →Utilizing Fair Value for Risk Management Purposes

Effective risk management requires timely recognition of emerging threats and opportunities. Fair value assessment plays a pivotal role by surfacing mark-to-market gains and losses, capturing fluctuations in interest rates, credit spreads, and commodity prices. Financial institutions, such as banks and asset managers, integrate fair value metrics into stress testing and scenario analyses, assessing capital adequacy under adverse scenarios.

Moreover, derivatives and structured products often mandate daily revaluation at fair value. This practice ensures counterparties maintain sufficient collateral and margin, mitigating counterparty credit risk. By embedding fair value assessment into risk dashboards, organizations can monitor exposures in real time, triggering risk limits or hedging actions when thresholds are breached.

Fair Value Assessment in Corporate Governance

Corporate boards and audit committees rely on fair value assessment to oversee management’s valuation judgments and ensure financial integrity. Transparent fair value disclosures reduce information asymmetry between insiders and external stakeholders, bolstering governance. Independent valuation experts and internal audit teams often review key assumptions, particularly for Level 3 inputs, where subjectivity is highest.

Effective governance frameworks mandate clear roles and responsibilities for valuation oversight. Policies outlining approved models, data sources, and escalation procedures help safeguard against manipulation. By embedding fair value assessment within governance structures, companies demonstrate commitment to reliable reporting and ethical decision-making, enhancing stakeholder trust.

Challenges and Criticisms Surrounding Fair Value Measurement

Despite its benefits, fair value assessment faces criticisms around subjectivity, volatility, and procyclicality. When markets become illiquid, observable inputs may disappear, forcing reliance on management’s projections. Such Level 3 estimations can be vulnerable to bias or “earnings management.” Stakeholders may question the reliability of valuations during extreme market stress.

Volatility in earnings and equity arising from regular remeasurements can also unsettle investors focused on stable returns. Critics argue that fair value accounting exacerbates market cycles by forcing fire sales in downturns. Addressing these concerns requires robust disclosures, sensitivity analyses, and governance to validate assumptions. Supplementary metrics, such as long-term value creation indicators, can complement fair value figures and provide a fuller performance picture.

Case Studies Demonstrating the Benefits of Fair Value Assessment

Numerous real-world examples highlight how fair value assessment drives better outcomes. During the financial crisis of 2008–2009, institutions with rigorous fair value frameworks identified distressed assets early, allowing proactive balance‐sheet management. Conversely, firms relying solely on historical cost struggled to recognize impairments until regulatory interventions mandated write‐downs.

In another scenario, a multinational corporation used income‐based fair value models to value complex intangible assets in an acquisition. The transparent methodology and sensitivity tables enabled both buyer and seller to reach a consensus, expediting deal closure. These case studies underscore fair value assessment’s capacity to uncover hidden risks and facilitate strategic transactions.

Conclusion: Harnessing the Power of Fair Value for Financial Success

Fair value assessment transforms static financial statements into living documents that reflect current market realities. By embracing its principles, techniques, and governance safeguards, organizations and investors can make more informed, timely decisions. The insights derived from fair value metrics support everything from portfolio construction and risk management to corporate valuations and strategic transactions.

As markets continue to evolve, mastering the art and science of fair value assessment will remain a competitive differentiator. Those who integrate rigorous valuation frameworks and transparent disclosures will build stronger stakeholder trust, better capitalize on opportunities, and navigate uncertainties with confidence.